Overall commercial property/casualty premiums increased slightly for all account sizes to 7% on average in the fourth quarter 2024, continuing a trend that has now last more than 6 years.

According to The Council of Insurance Agents and Brokers’ Q4 Market Survey, the 7% average increase in Q4 compared to 8.1% in Q3, is the 25th straight quarter with increases though. Almost all lines of business recorded smaller increases than in the previous quarter.

Respondents said not much had changed since last quarter, although some said competition had increased a bit for large accounts. These accounts saw overall average premium increases of 6.1%, which was the lowest among all account sizes.

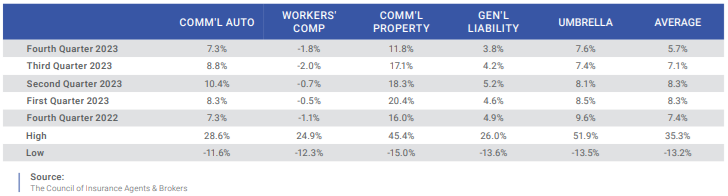

Increases in major lines of business—commercial auto, commercial property, general liability, umbrella and workers’ compensation—averaged 5.7% in Q4, down from 7.1% in Q3. Commercial property increases of 11.8% during Q4 continued a trend of moderation throughout 2023. Increases were 20.4% in Q1, 18.3% in Q2, and 17.1% in Q3.

According to respondents, reinsurance and natural catastrophe losses were given as reasons for increases in commercial property. Sixty-four percent of agents and brokers that answered the survey said there was a decrease in underwriting capacity. This marked the ninth quarter in a row that more than half of respondents said there was a decrease in capacity.

“At this point, we’re all numb to the changes and inundated with articles and whitepapers outlining the reasons,” said one survey respondent. “The underwriters and I have essentially stopped discussing the reasons and have moved on to individual account solutions at this point.”

In Q3 2023 D&O premiums decreased for the first time since Q1 2017. In Q4 2023, D&O increases were very nearly flat at 0.1%. Cyber increases dipped below 1% for the first time since the beginning of 2019, up 0.7%.

The Council noted that insureds’ rate fatigue and frustration with requests from carriers. Though down from the 70% mark recorded in Q3, 62% of agents and brokers said clients felt rate fatigue in Q4 and 55% felt burdened by requests for information from carriers.

On respondent said a client will attempt to improve its risk profile, but “the next year there are additional requirements,” and some feel they are “chasing a never-ending system where they have to make improvements to obtain coverage and then are hit financially both with improvements and premiums.”

Was this article valuable?

Here are more articles you may enjoy.

Navigators Can’t Parse ‘Additional Insured’ Policy Wording in Georgia Explosion Case

Navigators Can’t Parse ‘Additional Insured’ Policy Wording in Georgia Explosion Case  US Will Test Infant Formula to See If Botulism Is Wider Risk

US Will Test Infant Formula to See If Botulism Is Wider Risk  These Five Technologies Increase The Risk of Cyber Claims

These Five Technologies Increase The Risk of Cyber Claims  Berkshire Utility Presses Wildfire Appeal With Billions at Stake

Berkshire Utility Presses Wildfire Appeal With Billions at Stake

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.