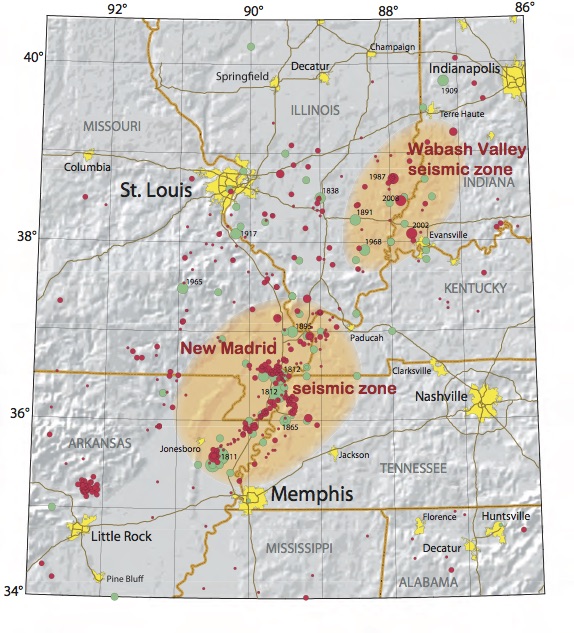

The Midwest’s New Madrid seismic zone is often eclipsed by San Andreas fault because of its less glamorous location and lower level of seismic activity, but our research indicates it’s a potentially crippling economic threat that warrants serious consideration.

The report, Four Earthquakes in 54 Days, estimates potential insured losses in today’s dollars, identifies factors that contribute to those losses and suggests how to be better prepared.

A complex peril

Unlike most earthquakes, which are characterized by a main shock and smaller aftershock sequence, the New Madrid earthquakes of 1811/1812 hit the central U.S. with a series of huge shaking events over a two month period. While records kept at the time chronicle the extraordinary effects on the landscape of a sparsely populated frontier region, there was little there to have been damaged. A vivid picture emerges when the same pattern of quakes is run through current-day models.

We calculate a series of quakes of the same magnitude today would cause $150 billion potential loss to the insurance industry, making it the costliest natural disaster to date. Including uninsured property and assets, total damage would be over $300 billion.

What makes the number so great?

The report considers a wide array of factors – seismic, demographic and economic – that come into play when modeling a peril of this scope.

Seismic: The region’s large-scale geological structure allows seismic waves to travel large distances with minimal loss of energy, plus its soft soil can exacerbate the duration and intensity of seismic shaking.

Demographic: The area has a population of 47 million, including five major metropolitan areas, placing a wide variety of residential and commercial buildings and infrastructure in harm’s way—much of it not built to withstand a strong earthquake.

Economic: Beyond physical damage, businesses would lose revenue while offline for an extended period. Demand for contractors and supplies would outrun supply, causing price inflation, and the claims handling process would be complicated by disputes over things like event definitions and deductibles.

Over one-third of our insured loss estimate is attributed to the multiple effects of large earthquakes occurring one after the other, something that wouldn’t be seen in a single, isolated earthquake. According to the report, multiple quakes will cause confusion as well as disagreement in handling insurance claims.

“This is based, in part, on recent experience of claims complexity and disputes following the 2010/2011 Christchurch earthquakes,” the report’s author writes. Not only will property damage coverage come into play but so will business interruption, demand surge and loss adjustment expenses.

Most insurers, reinsurers, rating agencies and policymakers are prepared for one large New Madrid earthquake, but it’s not at all certain that they’re prepared for more than one. The report notes that when there is seismic activity along the New Madrid fault line it tends to occur in “large event sequences” and would likely be of larger magnitude, closer in time and of greater economic value that in Christchurch.

Modeling points to damage that would be in a wider area with more moderate damage than seen in Christchurch.

The report’s analysis points out the need for better preparation, with much of the responsibility falling to insurers: understanding their capital requirements, developing effective claims protocols and encouraging greater take-up of earthquake insurance.

Source: Swiss Re

Was this article valuable?

Here are more articles you may enjoy.

Elon Musk Alone Can’t Explain Tesla’s Owner Exodus

Elon Musk Alone Can’t Explain Tesla’s Owner Exodus  Berkshire Utility Presses Wildfire Appeal With Billions at Stake

Berkshire Utility Presses Wildfire Appeal With Billions at Stake  China Bans Hidden Car Door Handles in World-First Safety Policy

China Bans Hidden Car Door Handles in World-First Safety Policy  Navigators Can’t Parse ‘Additional Insured’ Policy Wording in Georgia Explosion Case

Navigators Can’t Parse ‘Additional Insured’ Policy Wording in Georgia Explosion Case

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.