Hundreds of thousands of Americans already live in homes that have repeatedly flooded. To get a good handle on the extent of those losses, check out the Federal Emergency Management Agency’s web page that hosts an extensive dataset with information on structures that have had multiple National Flood Insurance Program (NFIP) claims.

Millions more people could be at risk by the end of the century as the seas continue to rise and extreme weather events become more common.

Unfortunately, inaccurate and backward-looking flood maps and the lack of disclosure of a property’s flood history leave homeowners, homebuyers and renters in the dark about their vulnerability to flooding. Outdated flood maps, or maps that fail to depict future flood risks, lead people to underestimate their danger. Lack of disclosure of past flood damages and other information hinders fully informed decision making, like choosing whether to buy flood insurance, and can lead to families being trapped in a nightmarish cycle of flooding, rebuilding, and repeating.

Related: Conflicting Policies May Cost Residents More on Flood Insurance, and Leave Them at Risk

Modernizing flood maps to show the future potential for flooding and requiring disclosure of past flood damages in real estate transactions could help people make better decisions about where they should live, how much they’re willing to pay to accept the risk that comes with a home, and other decisions. Maps should be more granular and accurate in their assessment of the potential for flooding and include projected future flood conditions. The more information a person has—and the better that information is—the better equipped they will be to avoid living in a flood-prone home or decrease their vulnerability to future floods.

Precise and Forward-Looking Flood Maps Key to Increasing Flood Resilience

For the U.S. to successfully adapt to sea level rise and flooding fueled by climate change, FEMA must develop more reliable flood maps that show where flooding is likely to occur both now and in the future. Currently, FEMA provides flood maps for 22,000 communities across the country. The maps provide the basis not only for who must buy flood insurance but also where FEMA’s floodplain management regulations apply.

Related: The Growing U.S. Flood Insurance Gap: A Wake-Up Call for the Industry

Due to these requirements, FEMA’s maps are the standard nearly everyone turns to. Developers, emergency managers and homeowners and buyers all rely on these maps for assessing and preparing for flooding. If FEMA’s flood maps are not accurate, communities will be misinformed about their true flood exposure.

Unfortunately, FEMA flood maps under-represent the true extent of the 100-year floodplain. Therefore, they under-represent the actual risks of flooding.

FEMA only maps the 100-year floodplain with a 50th percentile confidence. That means there is only a 50% chance that a 100-year flood would stay inside the line that FEMA draws on its maps. Basically, we are making development decisions with the certainty of a coin flip. We deserve better odds than that.

Related: Frequency of Deadly Hurricanes Has Jumped 300%

According to FEMA, NFIP policy holders who live outside the mapped floodplain, “file more than 25% of NFIP claims and receive one-third of disaster assistance for flooding.” Even worse, nearly 20% of the most flood-prone properties in the country (what FEMA calls Severe Repetitive Loss Properties, which have each flooded five times on average) also are located outside the floodplain, as currently delineated. Those numbers speak directly to the inadequacy of the flood maps we are using to guide all development decisions nationwide.

Mapping with a higher degree of confidence to show the true extent of areas vulnerable to flooding is a much-needed step in the right direction.

However, even if FEMA could rectify the mapping programs shortcomings, new maps still will not provide an accurate depiction of risk due to the absence of future conditions projections, like sea level rise, changes in rainfall and expected population growth.

For far too long, FEMA’s flood maps have defined flood risk based solely on past events. Historical storms are used to calibrate computer models that are used to map flood projections, on the assumption that the past should inform future decisions. Yet, by not taking climate impacts and other factors into account, communities are using bad flood maps to make even worse decisions about where it’s safe to build.

FEMA is now looking at how flood maps can incorporate information on future climate impacts. This would ensure that flood maps capture areas that are at risk today, as well as areas that will be under threat decades from now.

That’s important. Decades from now, we will still be relying on the homes, businesses and infrastructure that are built today. Making sure flood maps accurately portray those future risks is critical to making decisions that will stand up in the face of future climate impacts.

If these changing flood dynamics are not considered, communities may choose to locate development in areas that appear safe from flooding today but will be a flood disaster tomorrow. A Federal advisory committee, established to review and make recommendations to FEMA on how to improve the mapping program, specifically recommended such an approach. FEMA should follow through on the recommendations and enact policy changes that would require future conditions to be included on FEMA’s flood maps.

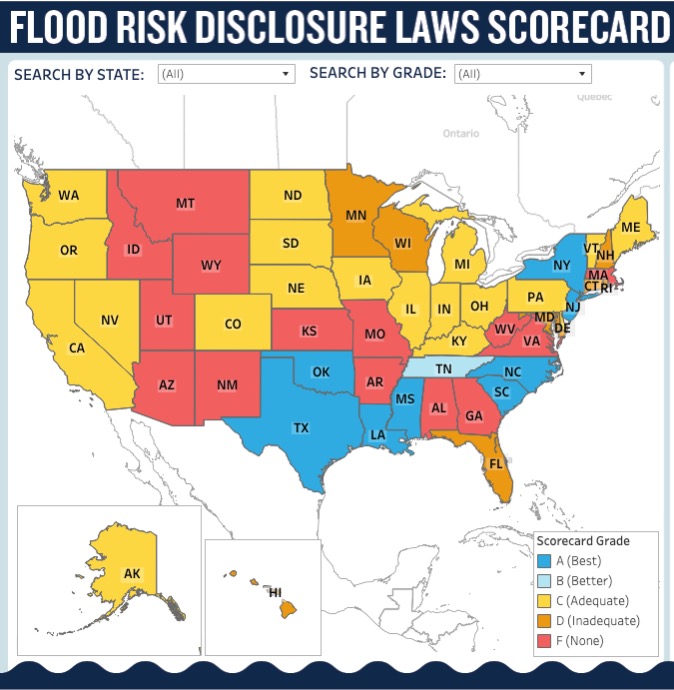

Strong Real Estate Disclosure Laws Needed

More precise and forward-looking flood maps are just one part of the safety equation. Everyone should have a right to know more than just whether a property is inside a mapped flood zone. They should also have a right to know a property’s flood history and flood insurance requirements.

Too many states have either inadequate or no statutory or regulatory flood risk disclosure requirements for home sales. Due to this lack of disclosure, homebuyers are not given the information that they need to make informed decisions about whether they should buy a house or purchase flood insurance. The purchase of a home is often a family’s biggest financial investment. Homebuyers deserve to know whether that investment is going to be underwater. If a seller knows, then it is only right the buyer does too.

For renters, the outlook is even more bleak. Only nine states require that renters be told whether a property is at risk of flooding. In 2024, Vermont became the ninth state by requiring landlords to inform prospective renters whether the property is in a FEMA-designated flood zone.

Inadequate disclosure laws mean far too many people have little knowledge of whether the place they may call home has ever flooded and thus, is likely to flood again. This problem could be solved simply by being told the truth about past flooding damages. Information that the seller or lessor of a home may have and should be required to provide a renter or prospective buyer.

Making sure information is passed from an owner to a seller or renter about flooding damages, legal requirements to purchase flood insurance and other risk information is justified because floods are costly. A homebuyer can incur tens of thousands of dollars in flood damage costs over the course of their mortgage, if they purchase a previously flooded home.

According to a study NRDC commissioned from the actuarial firm Milliman, 6.6% of all homes (28,826 homes) sold in 2021 in New Jersey, New York, and North Carolina, were estimated to have been previously flooded. For the individual homebuyer in North Carolina, the Milliman analysis found that over the life of a 30-year mortgage, buyers of a previously flooded home can expect to incur $36,328 in flood damages compared with homes that do not have a history of flooding. In New Jersey, homebuyers who purchase previously flooded homes can expect to pay $50,351 over a 30-year mortgage on average. In New York, the dollar amount is even higher. Homebuyers who purchase previously flooded homes can expect to pay $93,774 over a 30-year mortgage in comparison to a home that wasn’t previously flooded. Given the high cost of flooding, states should not keep homebuyers in the dark about a home’s flood history.

Strong real estate disclosure laws that require a seller to inform a buyer about a property’s flood history and risk would help address this problem.

However, such disclosure and transparency provisions should also not be limited to disclosure requirements imposed on sellers. The NFIP must also improve the information that is available to the public. Current homeowners who do have not the luxury of living in a state with good flood-hazard disclosure laws should have a right to know about their property’s flood risk. This should include any history of flood insurance coverage, damage claims paid and whether there is a legal requirement to purchase flood insurance because of past owners’ receipt of federal disaster aid. This is information that FEMA should have if a property was ever covered by the NFIP, and it should make it public and easily searchable by address. In addition, FEMA should provide greater access to a community or region’s flood risk information, such as aggregate claims and policy history, repeatedly flooded areas and whether NFIP-participating communities are complying with the requirements of the program.

People Deserve to Know Their Flood Risk

As sea levels rise and heavy rainstorms become more common, homeowners, buyers and renters deserve to know their vulnerability to flood when choosing where their family will call home. Transparency about flood damages and risks ensures that the market is not only fair (both sides of a transaction have the same information), but also is influenced by that information.

Homebuyers who have access to flood-risk information when browsing home listings online are more likely to view and make offers on homes with lower flood risk than those who don’t have access. In addition, knowing the level of one’s flood risk helps change patterns of behavior related to flood insurance, potentially increasing uptake of flood insurance policies. The more information people have about flooding, the better equipped they are for avoiding or mitigating the next potential disaster.

Scata focuses on issues related to preparing the U.S. for water-related impacts of climate change, including federal flood policy reform and adapting to sea-level rise. Prior to joining NRDC in 2014, Scata was a Peace Corps volunteer in Mali, working to conserve land threatened by desertification. He is based in NRDC’s Chicago office.

Was this article valuable?

Here are more articles you may enjoy.

US Will Test Infant Formula to See If Botulism Is Wider Risk

US Will Test Infant Formula to See If Botulism Is Wider Risk  Uber Jury Awards $8.5 Million Damages in Sexual Assault Case

Uber Jury Awards $8.5 Million Damages in Sexual Assault Case  China Bans Hidden Car Door Handles in World-First Safety Policy

China Bans Hidden Car Door Handles in World-First Safety Policy  Credit Suisse Nazi Probe Reveals Fresh SS Ties, Senator Says

Credit Suisse Nazi Probe Reveals Fresh SS Ties, Senator Says

Want to stay up to date?

Get the latest insurance news

sent straight to your inbox.